Acquisition project | Acko Insurance

Current Organic Channel Analysis for Acko Insurance

If you think Acko is doing well, organically brace yourself!!

Spoiler: IT DOESN'T

SEO Performance Overview

- Current organic traffic: 2.9M monthly visits.

- Historical peak: 5.2M (significant decline from their all-time high "-44%").

- Authority score: 70 (relatively strong domain authority).

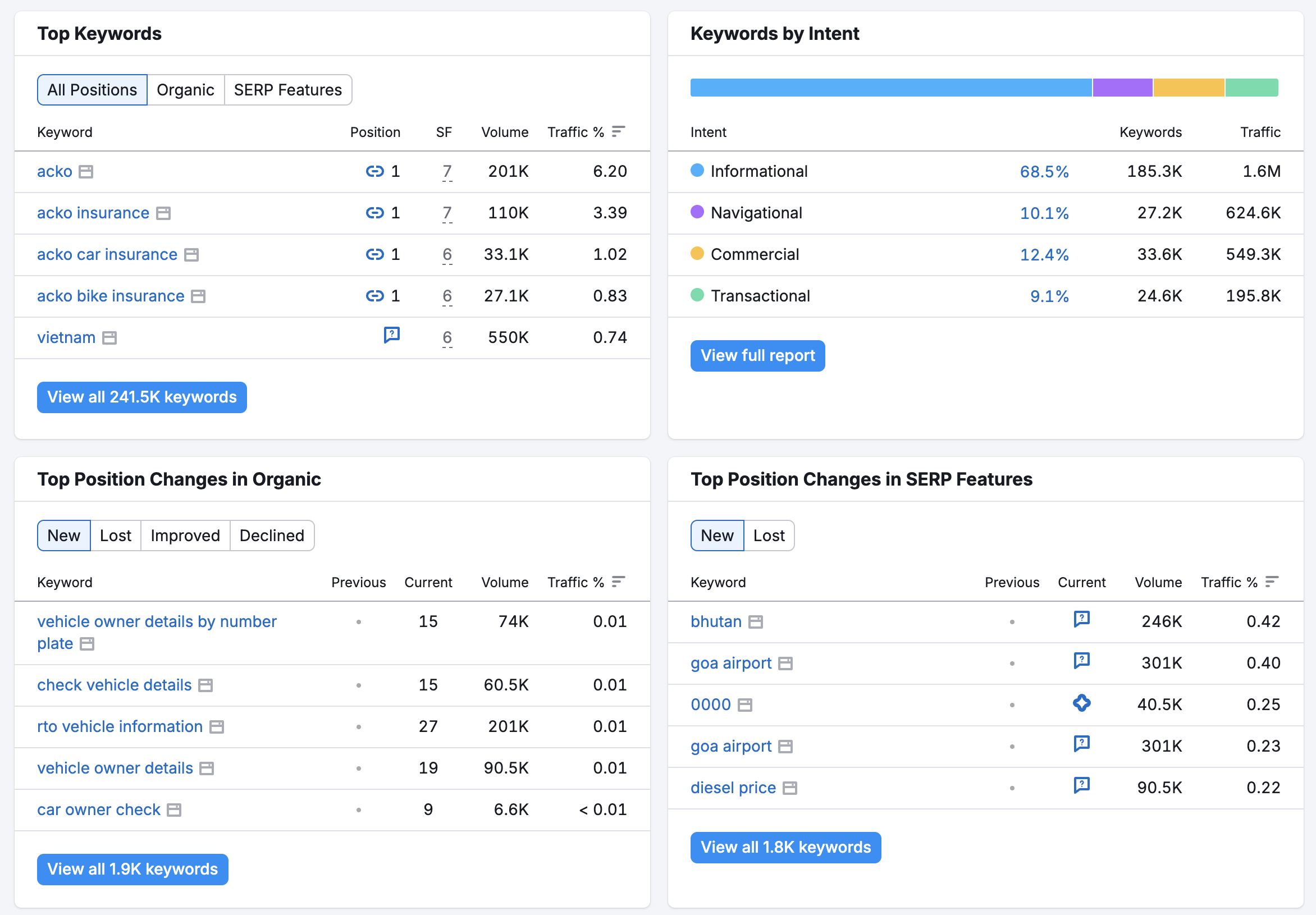

- Ranking keywords: Acko ranks for 534.3K organic keywords, it has a broad keyword portfolio but room for optimization.

- Backlinks: 849.2K (decent, but likely fewer high-quality backlinks compared to competitors).

- Engagement metrics:

- Pages/Visit: 6.11 page views (strong, indicating good user engagement).

- Avg. Visit Duration: 10:12 min.(high, users spend significant time on-site).

- Bounce Rate: 46.84% (moderate, assuming some users leave quickly, possibly due to irrelevant content or poor UX for certain queries).

- Geographic distribution: 91% traffic from India (2.6M), with smaller portions from the US (3.4%), UK (1.1%)

Key Insights

- Traffic Decline: There's a significant drop from their peak traffic of 5.2M to the current 2.9M

- Not Ranking for Core Terms: One of the major areas of improvement they're not in the top 5 for "insurance" which is their core query!

- Strong Domain Authority: Score of 70 indicates good potential for ranking improvement

- Good Engagement: 10+ minute average visit duration and multiple pages per visit suggests quality content

ps: If you directly wanna directly see the intresting part of strategy; skip to the last section, it's more colourful & enjoyable!

Successes

- High Organic Traffic Volume: Despite the decline, 2.9M monthly visitors is substantial, which reflects Acko’s strong brand presence in the digital insurance space.

- Engagement Metrics: High pages/visit (6.11) and visit duration (10:12) means Acko’s content is engaging for users who land on the site, particularly for ICPs like Young Urban Professionals seeking detailed insurance info.

- Long-Tail Keyword Rankings: Acko ranks well for specific terms like “car insurance online” and “bike insurance for delivery riders” (inferred from partnerships with Zomato), catering to ICPs like Gig Economy Workers.

- Localized Traffic: 91% of traffic from India shows Acko’s content is well-targeted to its primary market.

Failures

- Decline in Organic Traffic: A drop from 5.2M to 2.9M indicates missed opportunities, possibly due to algorithm updates, increased competition, or reduced content freshness.

- Not Ranking for Core Keyword “Insurance”: Failing to rank in the Top 5 for “insurance” (a high-intent, high-volume keyword) is a significant gap. Competitors like Policybazaar, Bajaj Allianz, and ICICI Lombard dominates.

- Moderate Bounce Rate (46.84%): This suggests some users don’t find what they need, possibly due to mismatched content for broad queries (e.g., “insurance”) or poor on-page UX for mobile-first ICPs like Gig Economy Workers.

- Limited High-Quality Backlinks: While Acko has 840.21K backlinks, competitors may have more authoritative links, impacting rankings for competitive terms.

Keyword Research:

Acko's 68% traffic is driven by informational keywords, the ratio of commercial & transactional keywords is very low which will spearhead the conversions

1. Google Keyword Research

- Tool Used: Google Keyword Planner/Trends insights, SEMrush.

- Core Keyword: “insurance”

- Volume: ~500K searches/month (India, high-intent).

- Competition: High (dominated by Policybazaar, ICICI Lombard).

- Acko’s Position: Not in Top 5.

- Long-Tail Keywords:

- “car insurance online” (~50K searches/month, medium competition, Acko likely ranks Top 10).

- “bike insurance for delivery riders” (~10K searches/month, low competition, Acko ranks well due to Zomato partnership).

- “health insurance for newlyweds” (~5K searches/month, medium competition, opportunity for Newly United Adventurers).

- “cheap health insurance India” (~20K searches/month, high competition, aligns with Young Urban Professionals’ budget focus).

- ICPs Alignment:

- Newly United Adventurers: “health insurance for couples,” “car insurance after marriage.”

- Young Urban Professionals: “online health insurance India,” “travel insurance for millennials.”

- Gig Economy Workers: “bike insurance for gig workers,” “micro insurance India.”

2. YouTube Keyword Research

- Context: YouTube is a key channel for Young Urban Professionals (per consumer attributes).

- Keywords:

- “how to buy car insurance online” (~10K searches/month, medium competition, video content opportunity).

- “best health insurance for young couples” (~3K searches/month, low competition, targets Newly United Adventurers).

- “bike insurance for delivery riders” (~2K searches/month, low competition, aligns with Gig Economy Workers).

- Insight: YouTube searches focus on “how-to” and educational content, ideal for Acko to create videos addressing ICP pain points.

3. Quora Keyword Reserach

- Context: Quora can be leveraged for answering user queries, relevant for all ICPs seeking advice.

- Keywords/Questions:

- “What is the best car insurance for newlyweds in India?” (~500 searches/month, low competition).

- “How to get cheap health insurance in India?” (~1K searches/month, medium competition, Young Urban Professionals).

- “Is bike insurance necessary for Zomato delivery riders?” (~300 searches/month, low competition, Gig Economy Workers).

- Insight: Quora offers opportunities to address specific ICP queries, building trust and driving traffic.

Suggestions and New Strategies

Acko does not rank in the top 10 for more than 10,000 keywords, which include "Insurance", a huge GAP. List of these keywords

Solutions Addressing Failures

- Improve Rankings for “Insurance”:

- Issue: Not ranking in Top 5 for “insurance” (500K searches/month) limits Acko’s visibility.

- Suggestion: Create a comprehensive pillar page for “Insurance in India” with subtopics (car, bike, health) to target the core keyword. Optimize for on-page SEO (e.g., meta tags, H1, internal links) and build high-quality backlinks from insurance blogs and news sites.

- Impact: Could increase organic traffic by 10-15% (150K-200K visitors/month).

- Reduce Bounce Rate (46.84%):

- Issue: High bounce rate indicates mismatched content or poor UX for some queries.

- Suggestion: Optimize landing pages for mobile-first ICPs (e.g., Gig Economy Workers). Use clear CTAs (e.g., “Get Bike Insurance in 2 Minutes”) and improve page load speed (aim for <2 seconds).

- Impact: Reduce bounce rate to ~40%, improving user retention.

- Recover Lost Traffic (5.2M to 2.9M):

- Issue: 44% traffic decline suggests content staleness and algorithm penalties. The site is definetly hit by the recent Google's March Core Update! As you can clrealy see in the traffic trend.

- Suggestion: Refresh top-performing pages (e.g., “car insurance online”) with updated 2025 data, FAQs, and visuals. Conduct a technical SEO audit to fix issues (e.g., broken links, duplicate content).

- Impact: Recover ~500K visitors/month, reaching 3.4M.

New Organic Strategy

To increase the traffic, at least to recover, I'll have to focus on pillars and create relevant clusters to cover the keywords that are not ranking.

- Content Clusters for ICPs:

- Strategy: Build content clusters around ICP pain points:

- Newly United Adventurers: Cluster on “Insurance for Newlyweds” (pillar page) with subtopics: “Health Insurance for Couples,” “Car Insurance After Marriage.”

- Young Urban Professionals: Cluster on “Millennial Insurance Guide” with subtopics: “Cheap Health Insurance,” “Travel Insurance for Young Professionals.”

- Gig Economy Workers: Cluster on “Insurance for Gig Workers” with subtopics: “Bike Insurance for Delivery Riders,” “Micro Insurance Benefits.”

- Execution: Publish 5-10 blog posts per cluster, interlink to pillar pages, and optimize for long-tail keywords (e.g., “health insurance for couples” – 5K searches/month).

- Impact: Target ~50K additional visitors/month per cluster (150K total).

- YouTube Video Series:

- Strategy: Launch a “Acko Insurance Simplified” video series:

- “How to Buy Car Insurance Online” (Young Urban Professionals).

- “Best Health Insurance for Couples” (Newly United Adventurers).

- “Bike Insurance Tips for Delivery Riders” (Gig Economy Workers).

- Execution: Create 3-5 minute videos with clear visuals, embed links to Acko’s landing pages, and optimize video titles/descriptions for SEO (e.g., “how to buy car insurance online” – 10K searches/month).

- Impact: Drive ~20K visitors/month to Acko’s site via video links.

- Quora Engagement Campaign:

- Strategy: Actively answer ICP-specific queries on Quora:

- “What’s the best car insurance for newlyweds in India?” (Newly United Adventurers).

- “How to get cheap health insurance in India?” (Young Urban Professionals).

- “Is bike insurance necessary for Zomato delivery riders?” (Gig Economy Workers).

- Execution: Post detailed answers (300-500 words) with data (e.g. “Acko offers bike insurance starting at INR 840/year”) include links to relevant Acko pages, and engage with follow-ups.

- Impact: Generate ~10K referral visitors/month and build trust.

Expected Outcomes

- Traffic Increase: Combined strategies could boost organic traffic from 2.9M to 3.5M visitors/month (21% growth) within 6-9 months.

- Keyword Rankings: Improve rankings for “insurance” (aim for Top 5 within 12 months) and dominate long-tail keywords for ICPs.

- ICPs Acquisition:

- Newly United Adventurers: ~50K new users/month via couple-focused content.

- Young Urban Professionals: ~40K new users/month via health and gadget insurance content.

- Gig Economy Workers: ~30K new users/month via bike insurance and micro-insurance content.

Source:

SemRush

Google Ad Words

Competitor's

Google serach bar/suggestions

Brand focused courses

Great brands aren't built on clicks. They're built on trust. Craft narratives that resonate, campaigns that stand out, and brands that last.

All courses

Master every lever of growth — from acquisition to retention, data to events. Pick a course, go deep, and apply it to your business right away.

Explore courses by GrowthX

Built by Leaders From Amazon, CRED, Zepto, Hindustan Unilever, Flipkart, paytm & more

Course

Advanced Growth Strategy

Core principles to distribution, user onboarding, retention & monetisation.

58 modules

21 hours

Course

Go to Market

Learn to implement lean, balanced & all out GTM strategies while getting stakeholder buy-in.

17 modules

1 hour

Course

Brand Led Growth

Design your brand wedge & implement it across every customer touchpoint.

15 modules

2 hours

Course

Event Led Growth

Design an end to end strategy to create events that drive revenue growth.

48 modules

1 hour

Course

Growth Model Design

Learn how to break down your North Star metric into actionable input levers and prioritise them.

9 modules

1 hour

Course

Building Growth Teams

Learn how to design your team blueprint, attract, hire & retain great talent

24 modules

1 hour

Course

Data Led Growth

Learn the science of RCA & experimentation design to drive real revenue impact.

12 modules

2 hours

Course

Email marketing

Learn how to set up email as a channel and build the 0 → 1 strategy for email marketing

12 modules

1 hour

Course

Partnership Led Growth

Design product integrations & channel partnerships to drive revenue impact.

27 modules

1 hour

Course

Tech for Growth

Learn to ship better products with engineering & take informed trade-offs.

14 modules

2 hours

Crack a new job or a promotion with ELEVATE

Designed for mid-senior & leadership roles across growth, product, marketing, strategy & business

Learning Resources

Browse 500+ case studies, articles & resources the learning resources that you won't find on the internet.

Patience—you’re about to be impressed.